5 Factors Impacting Pharmaceutical Healthcare Industry Transformation

What is going on in 2018 with healthcare in AmericaThe health care industry in the United States is experiencing major challenges, from the financial debacle besieging the hospital and health care sector to lack of transparency regarding PBM revenue and prescription drug pricing, change is needed and projected to be on the way.

Are Jeff Bezos and Tim Cook ready to join the ranks of health system CEOs? Perhaps. As a market disruptor, Amazon and Apple are the gold standard.

Now involved in the health care field, each is poised to have an impact on the American health care industry. Across the world today, innovative technologies are center stage, impacting most aspects of daily life. Why should health care be any different? From Bluetooth-enabled medical devices to 3-D printing, technology advancements are making human life easier and more comfortable.

With the open enrollment of health insurance approaching fast, let’s take a look at 5 factors that are having a major impact on the pharma healthcare industry.

1. Amazon

Healthcare stocks plummeted with the news. PBM Express Scripts stock declined nearly 9% and CVS and UnitedHealth stock fell more than 4% in early trading. Humana and Walgreens experienced more than a 3% drop.

A mere five months later, the other shoe dropped. In late June 2018, Amazon announced the acquisition of PillPack, a thriving online pharmacy business. PillPack specializes in prescription drug mail order fulfillment. Their prescription for success lies in their ability to provide single-dose pill packs which make it easier for patients who are required to take doses of multiple medications. By pre-sorting medications into individual, clearly labeled daily dose packaging and delivering them directly to patients, PillPack found a winning formula and fulfills a critical need in the industry for patients.

Why did Amazon acquire PillPack? No great mystery. One of the company’s greatest assets is that it is licensed to sell prescription drugs in 49 states. In addition, PillPack also provides drug products through PBMs including Express Scripts, CVS Caremark and Optum Rx. Acquiring licenses is time consuming, costly and labor intensive. The acquisition of PillPack enables Amazon to take a shortcut and fast track the process.

2. Major Challenges in the Healthcare Industry

To be clear, there are many challenges in today’s healthcare system and industry. Here are a few that are having a major impact.

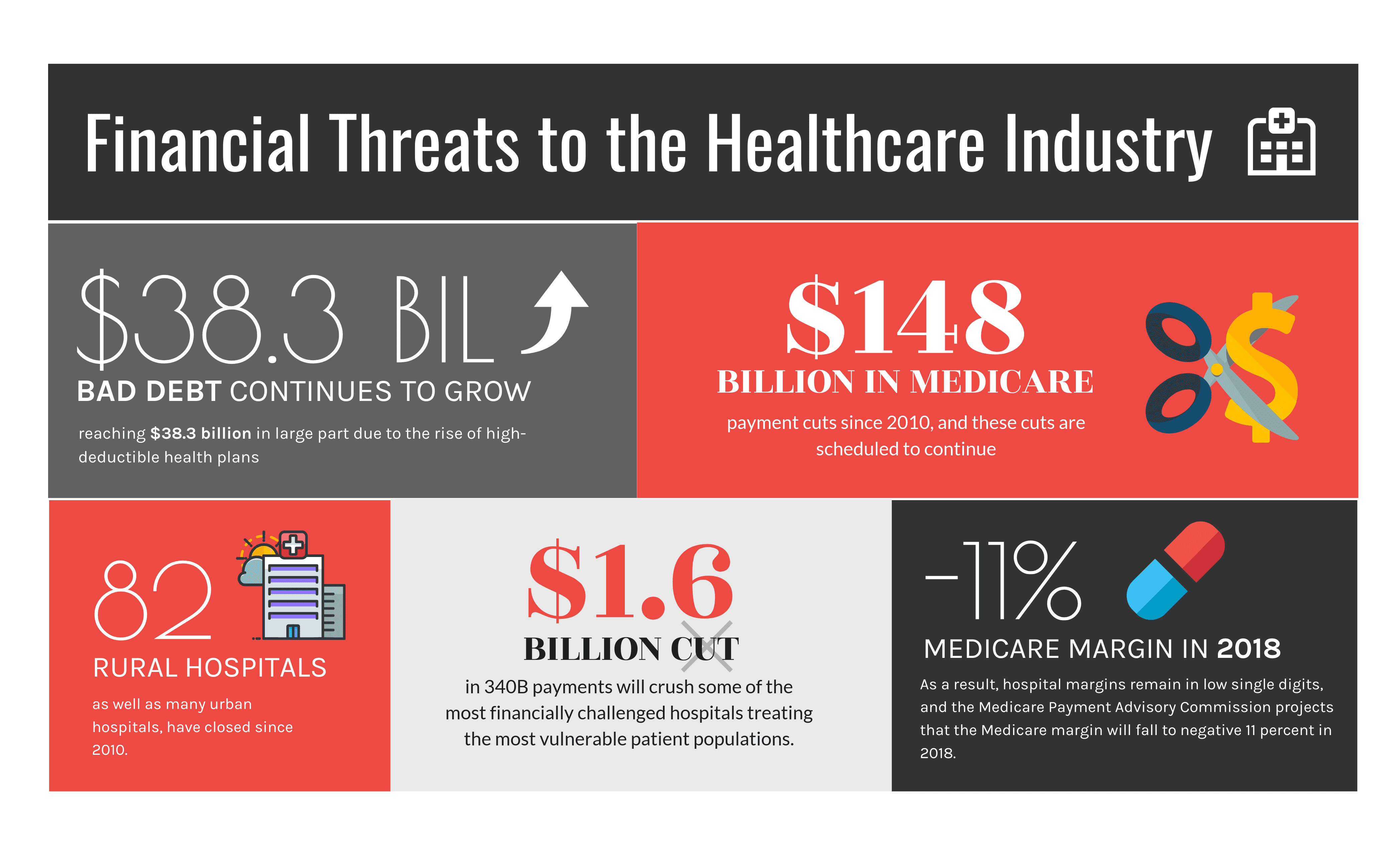

Rising costs and an uncertain regulatory climate are hampering profitability in this sector. In addition, hospitals are struggling with the escalation of bad debt. One factor at issue with hospital bad debt is known as the Patient Balance After Insurance, PBAJ. This is the amount that patients owe to hospitals after the medical insurance portion has been deducted. Due to the rising cost of health insurance, many consumers are forced to take medical insurance policies with higher deductibles, leaving them vulnerable to debt. PBAJ increased from 8% of total bill responsibility during Q1 of 2012 to 12.2% during the same quarter in 2017. Patients with commercial insurance realized an increase of 67% in PBAJ which consequently helped to propel total hospital revenue attributed to PBAJ 88% in that five-year period.

Then there is the issue of Medicare Bad Debt which occurs when Medicare patients fail to pay their deductibles. Within the time frame of 2012 to 2016, Medicare Bad Debt increased 17%. Hospitals tend to collect approximately 65% of this cost from Medicare if they can document that they exhausted all efforts to collect from the Medicare beneficiary, a loss of 35%.

Additional financial threats to the hospital industry are occurring across the country. 82 rural hospitals as well as many urban hospitals have closed since 2010. In 2018, $1.6 billion reduction in 340B payments will devastate hospitals that are already financially susceptible to failure. These financially precarious hospitals are servicing vulnerable patient populations. Because hospitals tend to be disadvantaged in the architecture of many of the pay-for-performance and alternative payment models of the Centers for Medicare and Medicaid Service (CMS), hospital margins are in the single digit margins. The Medicare Payment Advisory Commission forecasts that the Medicare margin will drop to negative 11% in 2018.

PBM Pricing Challenged

Complaints about the lack of transparency involving PBM profitability and business practices have gotten attention. At the onset, PBMs reduced costs by aggregating health plan consumers, creating large networks that provided them with increased buying power to negotiate discounts. Industry consolidation, power and lack of transparency have changed the cost savings equation, however. Today the top three PBMs, CVS Caremark, Express Scripts and OptumRx control 85% of the market. In order to have the drugs they produce included on PBM formularies, manufacturers often increase the cost of the prescription drugs to pay considerable rebates and fees to the PBMs. The result is an outcry about lack of transparency involving how PBMs generate revenue and calls for industry oversight.

Many factors impact revenue generation for Pharmacy Benefit Managers. For example, PBMs have leverage over prescription decisions due to their involvement in pre-authorization requirements. Another way that PBMS generate revenue involves billing health plans for amounts higher than they reimburse pharmacies, creating a “pharmacy spread”. In addition, PBMs impose “direct and indirect renumeration” (DIR) fees on pharmacies, imposed after sale in a manner that in not readily predictable. To restrict the availability of lower cost options, PBMs use “gag clauses” with pharmacists to prevent them from informing consumers about lower cost options for prescription drugs. Another PBM strategy is the practice of “clawbacks”, patient reimbursement higher in copayments than the actual cost of a drug. This has enabled PBMs to be able to create streams of protected revenue away from public view.

Issues such as clawbacks, DIR fees and gag clauses are currently legal. There is no oversight or public disclosure to determine if PBMs are actually producing cost savings. Additionally, there is currently no regulation or obligation to eliminate conflict of interest. CVS Caremark, for example encouraged patients to switch pharmacies and simultaneously decreased reimbursement to rival pharmacies.

Rising Costs of Medical Insurance: Consequences of Changes to the Affordable Care Act (ACA)

Repeal of the Individual Mandate in Obamacare

The Tax Cuts and Jobs Act signed into law in 2017 repeals the individual mandate, the ACA tax on individuals who fail to secure health insurance.

Termination of Cost Saving Reductions (CSR)

Billions of dollars of payments subsidizing health care costs for lower-income consumers known as Cost Saving Reductions (CSR) were terminated by Executive Order in October 2017. Because CSRs are passed from the federal government to the insurer and directly to the patient, this reportedly will negatively impact consumers rather than insurers and increase the cost of medical insurance. The move has been anticipated to cause instability in the healthcare insurance market and increase costs.

3. Transition to Value-Based Programs

Developed by CMS, the Centers for Medicare and Medicaid Services, value-based programs work by rewarding health care providers with incentive payments to provide the highest quality health care for the lowest cost. This will replace the current fee-for-service model. As of 2018, 90% of traditional Medicare payments are required to be tied to quality or value.

Value-Based Purchasing (VBP)

Moving from the fee-for service compensation model in which reimbursements are made for each service provided without regard to patient health outcome or cost, the value-based purchasing model refers to a range of payment strategies linking provider performance and reimbursement.

Value-Based Care

Designed to improve the quality of patient health care and more efficient and cost-effective use of resources, value-based care helps to ensure improved health outcomes for patients. While payments for services are still distributed by medical insurance companies, Medicare or Medicaid, healthcare providers are paid based on how healthy they are able to keep their patients. Value-based care emphasizes the quality of health care rather than the quantity of care.

Value-based care relies on a team approach. Headed by a primary care physician who coordinates care, a team of healthcare providers and other resources collaborate to treat each individual patient.

Value-Based Drug Pricing

Pressured to reduce the cost of prescription drugs, the pharmaceutical industry is turning to value-based contracts, linking the pricing of drug products to their clinical or economic performance. Growing demands for cost control require closer collaboration between pharma life sciences organizations, health care systems, insurers, PBMs, patients and healthcare providers.

Technology is lending a helping hand to this effort. Advances in cloud-based technologies as well as regulatory trends are enabling easier capture of clinical and financial impacts of new therapies in the real world.

4. Vertical Integration in Healthcare

The healthcare industry is seeing advancement toward the continued focus of CMS paying for value-oriented models. The Medicare Access and CHIP Reauthorization Act of 2015 incentivizes clinicians to take risks and spurring action for alternative payment models (APMs). In the private sector, actions are being taken to expedite the value-based payment movement and disrupt the current fee-for-service model.

Forces in and outside of the healthcare industry are re-organizing the market, vertically integrating healthcare providers and payers into high-value care and financing networks including ownership models or partnerships. Now that there are clear signals that the value-based model is moving forward, those in the healthcare industry are concentrating on gaining scale, vertically-integrating or partnering to improve their market position and position themselves for the expansion of value-based care.

One of the primary reasons for the activity in merger and acquisition and vertical integration

With new health care delivery networks emerging, the industry is scrambling. To meet the new value-based models, new capabilities, integrations have been developed, new networks created and the means to collect, integrate and use data are needed. With the expectation of producing the means for more patient outcome-focused care at high quality at lower cost, 2018 is a year of focus on patient engagement to aid in enabling patients to better manage their personal health and health care.

Here are some of the most notable vertical-integration deals:

Seeking to be more competitive in a crowded, challenging marketplace, medical insurers, health systems, physician groups

5. Technology and Healthcare

Managing Healthcare and Pharmaceutical Inventory

From the need to comply with FDA regulations to the complex challenges of handling, storing and shipping life sciences goods in today’s fast-paced world necessitates RFID or automated data collection methods to provide real time data visibility, streamline operations and reduce waste and costs. Managing the pharmaceutical and healthcare supply chain today requires the use of technology.

Supply chain management software such as warehouse management systems are now the norm in the industry. Today software and systems technology are used to improve the patient experience. This includes patient connection and engagement systems, used to enhance patient-centric care.

Big Data, Predictive Analytics

Capturing real time data is essential for the modernization of the healthcare system. Using data from diverse sources such as electronic medical records (EMRs), pharmaceutical and health care warehouse operations as well as other sources is being used with innovative new technologies including artificial intelligence, predictive analytics and machine learning to optimize pharmaceutical outcomes and enable better real time decision making and new processes and solutions for the healthcare industry.

Innovative New Technology-Oriented Therapies, Diagnostics and Devices

Consumers have embraced technology. Technology innovators are finding new ways to focus on home health using consumer-oriented devices as well as innovative and familiar technologies. Imaginative tech innovations are helping to cut costs, improve patient care, improve the safety and comfort of patients and much more. Technology is truly poised to enhance the health care experience.

Medical researchers have even worked to determine how to reproduce human cells using 3-D printing technology and this technology has been used to create prosthetic limbs, artificial skin and more. Review of global health care industry trends reveal that the healthcare industry is undergoing significant upheaval and transformation and favors expanded use of innovative and emerging technologies. Can you imagine what new ideas and technological advancements will be available in 5 or 10 years? It seems to defy the imagination.

Conclusion

Rising health insurance and pharmaceutical cost are propelling transformative changes in the pharma healthcare industry. Gone are the days of paper folders and files. Today, the need to improve the quality and cost of patient care services requires that all parties involved in patient care have access to the same, accurate information. Use of electronic health records has facilitated greater ease and collaboration of healthcare providers, healthcare facilities and others in the health care sector that provide patient care.

Industry consolidation, mergers and acquisitions and vertical integration is re-shaping the industry, giving rise to entirely new types of competitors in the market.

What Makes Datex Different?

1. Revolutionary low code/no code flexible workflow-driven warehouse management software

2. Most configurable, user-friendly WMS on the market today

3. End-to-end solution provider: software, hardware, EDI, and managed services

4. White Glove Concierge Service

5. Executive-level attention and oversight