2018 3PL Refrigerated Warehouse Cold Chain Industry Trends

Cold Chain Industry 2018 Trends Including Refrigerated WarehousingThe cold chain industry is changing fast. Between the increased development and usage of temperature sensitive biologic pharmaceuticals and consumer preferences for convenient, fresh foods, the cold chain must adapt quickly.

One main factor is dominating the cold chain these days: the power of consumers. Today’s consumer values convenience, wholesome food

Moving away from highly processed foods with a long shelf life to temperature-sensitive perishable food products requires an adjustment in the food supply chain. Because consumers value convenience and fast delivery, there are added complications. From U.S. ports to distribution centers, 3PLs and privately owned refrigerated warehouses, designing a cold chain that meets consumer needs can seem daunting.

The Future Looks Bright for Refrigerated Warehouses & the Cold Chain Industry

Consumers Drive Growth in Cold Chain Industry

The sheer number of consumers has increased across the world in recent years and continues to expand. Consumers value convenience, quality, service and

Today’s consumers, especially Millennials, expect variety. Variety=more and more SKUs as food manufacturers add new packaging types, flavors, sizes and other options. Because of the desire for fresh food products in increasing variety and need for convenience, food producers and manufacturers are altering what they are producing, where it is being produced and how it is distributed and transported to the door of consumers. More fresh and chilled products are being ordered in smaller quantities from a wider range of product choices. This is causing a proliferation of new product development, product and packaging changes and updates.

Consumers crave information about the products they purchase and use their Smartphones, tablets and other devices to find and share information and their opinions on social media. This

When it comes to food, 2017 was one of the most important years in history. The food and grocery industry is changing at breakneck speed, due to consumer buying habits and expectations. The food industry is changing faster than the supply chain can accommodate it. In less than 2 years, 17 CEOs of major food companies left their positions and were replaced by more “fresh-thinking executives”. The food industry is searching for a new consumer-centric retail model and the design of this new paradigm impacts the cold chain industry.

Consumer buying preferences have changed markedly. Today’s consumer prefers freshly

Setting up regional supply chain networks, accessing regional transportation routes and temperature-controlled logistics and warehouses is vital and transformative.

Consumers’ hunger for convenience helped create the meal-kit industry, a new menu item for today’s busy consumer. Now even Walmart has entered the cutthroat industry, competing with industry giant Amazon in the grocery wars. Add to this the proliferation of restaurant delivery mobile apps and the party is just starting to heat up.

What does all of this mean for cold storage warehouses? Better buckle up Buttercup. It’s likely to be a bumpy ride. No longer will refrigerated warehouses be able to exclusively enjoy the simplicity of pallet in-pallet out operations. The cold chain needs to change and must become as flexible and transparent as possible and that will take technology, forward-thinking business executives

Increase in Need for Refrigerated Warehousing of Temperature-Controlled Pharmaceuticals.

Of the 57 new drug approvals issued by the FDA in 2017, 28 of the 57 are temperature-sensitive products with 23 requiring refrigeration storage and transportation. Five additional products require cryogenic (below-zero) temperatures. In the 2017 Cold Chain Outlook produced by Pharmaceutical Commerce Magazine, the global volume of 2017 cold chain products is estimated to be $283 billion and is growing at twice the rate of the overall pharma market.

Biologic drugs as well as the manufacturing process involved with

Another trend increasing the need for pharmaceutical product refrigeration is the evolution of a variety of precision medicine innovations that range from cellular therapies to biomarker testing, regenerative medicines that use stem cells.

Some of the therapies involve extracting tissue or blood from patients which must then be transported to a facility for some type of genetic or other manipulation then returned to the patient. Each step in this type of therapeutic process is potentially a cold chain task, requiring stringent constraint on monitoring the condition of the shipment. Use of temperature monitoring electronics, insulated containers, refrigerants and other logistics practices are needed to ensure safety in human use.

The nature of many pharmaceutical and life science products makes it necessary to transport, handle and store them within an established temperature range. In some instances, new technology products are required when dealing with specific products, such as data loggers to monitor the storage temperatures of vaccines.

Expansion of Value-Added Services

3PL cold storage operators are optimizing the utilization of their assets. Because refrigerated warehouses are especially expensive to build and operate, extending services beyond merely handling and storing products makes perfect economic sense. Providing an array of value-added services also serves to help build a partnership between the 3PL and its customers.

According to the International Association of Refrigerated Warehouse’s 2016 Productivity and Benchmarking Survey, 56% of the revenue recognized by the cold chain industry comes from non-storage activities. Today’s multi-temperature warehouse customer is more likely to outsource work such as logistics management, repacking, labeling, packaging and other activities to save money and reduce the burden on their operations. Third party warehouses are also providing light processing to reduce the burden on food producers and manufacturers.

By shifting the cost of the warehouse investment from the customer to the 3PL, it can be spread across multiple customers. Value-added services provide additional incentive for customers to select the refrigerated warehouse operator and help reduce their overall expenses. In selecting a public cold storage warehouse, 3PL customers also benefit from the economies of scale, have a lower point of entry to the temperature-controlled supply chain and have access to already developed delivery networks and do not need to invest heavily in systems, technology and logistics expertise.

In addition to providing

For some 3PLs, however, the complexity of billing for value-added services for many different customers, inventory types, activities and metrics means that they are missing out on revenue.

This typically occurs for 3PL cold storage operators that are not using WMS software with 3PL billing capabilities, using legacy systems or using systems not specifically developed to meet the needs of third party logistics providers. Just as with other issues in warehouse operations and inventory management, having the necessary tools can make a major impact on profitability.

Labor shortage

Across the supply chain industry, businesses are reporting that they are suffering from a shortage of qualified candidates to fill essential positions. Whether it is a warehouse worker, truck driver, IT or operations professional, the lack of labor diminishes the capabilities of the business. According to industry experts, because many shippers have been outsourcing warehouse and transportation to 3PLs, they may not be aware of the extent of the labor shortage and the challenges this poses to the supply chain. This presents new opportunities for

As labor pools tighten, many supply chain operations are looking towards technology for help in filling the gap. Because of the new focus on technology, workers need increased training. Whether dealing with providing new services or last mile delivery, cold chain workers need to become more skilled to meet these higher expectations.

According to industry experts, much of the funds projected for investment in cold storage and other building projects

Increased Adoption of Innovative Technologies Including Robotics and Automation

Warehouse automation, originally popular in Europe where labor and land are more expensive, is now reaching more widespread adoption in North American cold storage warehouses. Several factors are combining to increase the adoption of new technologies:

- Shortage of refrigerated warehouse workers

- Worker safety, comfort and employment longevity issues from exposure to intense cold temperatures

- Availability and cost of new technologies that can streamline efficiency and replace manual work

- Need for increased speed and accuracy of operations

- Desire to optimize storage within the available facility footprint

- Need to decrease waste and product damages

- Ability to reduce overall costs, especially energy expenses and cold loss

- Impact of recent U.S. tax cut

Private and public refrigerated warehouses have been replacing existing systems used in routine packaging and palletizing with automated systems. Many multi-temperature warehouse operators have shown an interest in adopting AS/RS warehousing.

Accelerated Inventory Turns

According to cold chain industry experts, long-term storage now accounts for a fraction of total warehouse income in many facilities. To improve inventory turn velocity, shippers are often relying on a Just-in-Time (JIT) strategy. This utilizes

Cold storage warehouse operators that rely on

Environmental and Sustainability Concerns

Whether it originated from consumer sentiment or the need to simply cut costs, cold storage warehouse operators have become increasingly aware of energy and water consumption. Many 3PL and private warehouse operators have adopted enterprise-wide sustainability initiatives, including:

- Building features designed for longevity and sustainability

- Utilizing alternative refrigeration options such as NH3, low charge and fluorocarbon-based systems

- Reducing dependence upon HCFC refrigerants

- Implementing reclamation, recycling and re-use programs

- Following S. Green Building Council (USGBC) LEED guidelines

- Implementing energy management plans to reduce energy use and cost

- Ensuring that supply chains are able to be flexible, stable and capable of moving the appropriate amount of goods to the correct locations at the right time is essential in meeting consumer expectations and reducing waste and damages

By anticipating demand, supply chain operations can be better positioned geographically to serve the end consumer. Because the products handled and stored in refrigerated warehouses are subject to spoilage, damage and diminished quality and value, getting the goods to consumers quickly is essential. Being able to tailor production and distribution to meet demand can reduce product waste and quality reduction that can lead to food safety issues.

Food Safety Issues

According to estimates from the Centers for Disease Control and Prevention (CDC), foodborne illnesses cause approximately 1 in 6 Americans (48 million people) to get sick. Of these, 3,000 people die and 128,000 are hospitalized from foodborne diseases. Issues regarding food safety have increased in number and at times, in complexity. Factors impacting the increased numbers of product recalls include but are not limited to:

- New FDA Food Safety Modernization Act (FSMA) mandated track and trace documentation of third party product suppliers

- Undeclared allergens in food products

Incidence of foodborne pathogens- Misbranding and mislabeling

- Inadequate or lack of pasteurization documentation

- Counterfeit food products

- Consumer expectations

To protect consumers, there is an enhanced need for worker safety training as well as for air quality testing, swab tests for listeria and a greater focus on efficiency to safeguard the quality of food products. Another major issue in food safety involves the cold chain itself. Perishable goods are subject to biological decay processes. Delivering perishable goods that are safe and of acceptable quality requires that the products are maintained within the appropriate specific temperature range during transportation and storage. Cold chain industry studies show that this remains challenging. Problems with precooling, transportation ground operations, commercial handling practices

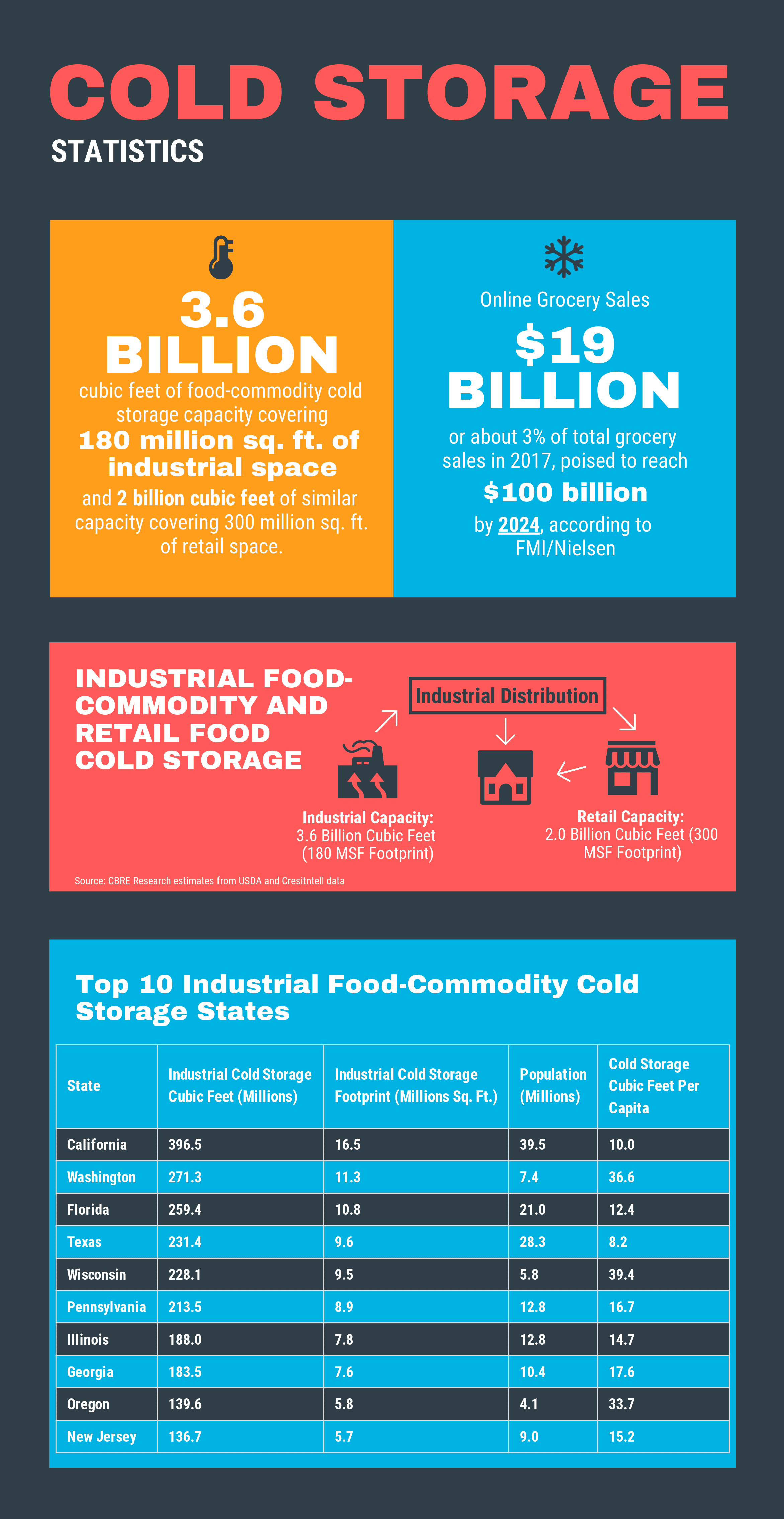

Growth in Online Grocery Sales Anticipated to Increase Demand for Cold Storage Warehouse Space

The acceleration of consumer demand and increase in e-commerce grocery sales is expected to fuel demand for more refrigerated warehouse space. According to real estate experts at CBRE, the increase in online grocery sales is set to disrupt food product storage and home delivery.

As consumers gain more confidence from positive experience shopping online, grocery retailers are exploring new options to increase online grocery sales. Designed to reduce concerns regarding spoilage and diminished product quality, the new models include refrigerated lockers at terminal stations, instant delivery service with a one to

In a January 2017 report by Nielsen regarding a study by Nielsen Global E-Commerce, 4% of North American consumers surveyed regularly have purchased fresh and household groceries online, 6% have made these online purchases in the past but not recently and 36% are considering this in the near future. According to FMI/Nielsen, online grocery accounted for nearly 3% of total grocery sales in 2017, approximately $19 billion. Online grocery sales are anticipated to reach $100 billion, 13% by 2024, only 6 years from now.

According to the Global Cold Chain Alliance (GCCA), the average occupancy rate of a cold storage warehouse currently exceeds 85%. Most industry experts consider that to be a “full” facility. Currently, there is 3.6 billion cubic feet of food-commodity cold storage capacity within 180 million square feet of industrial space, primarily in refrigerated warehouses as well as approximately 300 million square feet of space in grocery stores and other types of retail venues. The growth of online grocery sales has the potential to increase the demand for approximately 35 million square feet of U.S. based cold storage space, moving from retail stores to warehouses and distribution over the span of the next seven years.

To reduce costs and time of delivery to consumers, often refrigerated warehouses are situated near densely populated areas. The high cost of cold storage warehouse construction and ongoing operation, escalating land prices and capacity constraint

Cold Storage Industry Consolidation Continues

With more than 600 refrigerated warehouse operators across the United States, the cold storage warehouse industry is dominated by the top 10 companies which own 80% of the market. This trend is poised to continue as the largest enterprises merge or acquire smaller cold storage warehouse operations.

Although some major food retailers own their distribution, others

Centers of Consolidation are Ideal Locations for Cold Storage Warehouses

As most of the food and grocery industry is low margin, keeping costs down is paramount. Food producers, manufacturers, retailers and 3PLs are continuing to work together to find ways to reduce costs. One way is to use centers of consolidation for import or export-oriented facilities. The idea is that the longer that the majority of products can be stored and transported together, the better the cost benefit. Processing the bulk of a product in one location prior to distribution or having it inspected in one location saves time and money. Centers of consolidation are often traced back to the chain of responsibility, such as an infrastructure center such as a port.

Conclusion

What is going on in the cold chain this year?

Consumers are driving change and growth in the cold chain industry. This means SKU proliferation, faster inventory turns and an increased need for

Development and adoption of innovative new temperature-sensitive biologic pharmaceuticals

The labor shortage continues and the investment in new technologies to

Cold storage warehouse operators have become increasingly aware of and invested in reducing energy consumption and adopting sustainable operations.

The continued incidence of foodborne illness is a major issue in the cold chain industry. Problems with insufficient worker training, precooling, transportation ground operations

The projected increase in online grocery sales is fueling demand for more cold storage warehouse space. An FMI/Nielsen report indicates a projected pattern of growth from $19 billion to $100 billion by 2024. Current U.S. cold storage warehouse occupancy rates already top 85%.

Location of refrigerated warehouses tends to be near population centers, agricultural areas and at or adjacent to centers of consolidation. This is to reduce transit time to consumers and take advantage of ways to reduce cost.

The cold storage warehouse industry remains dominated by the top 10 operators which own 80% of the market.

Do you have an issue with 3PL billing? Take a look at our 3PL WMS Billing Guide.

What Makes Datex Different?

1. Revolutionary low code/no code flexible workflow-driven warehouse management software

2. Most configurable, user-friendly WMS on the market today

3. End-to-end solution provider: software, hardware, EDI, and managed services

4. White Glove Concierge Service

5. Executive-level attention and oversight